The 20% Down Payment Myth, Debunked

The 20% Down Payment Myth, Debunked

Saving up to buy a home can feel a little intimidating, especially right now. And for many first-time buyers, the idea that you have to put 20% down can feel like a major roadblock.

But that’s actually a common misconception. Here’s the truth.

Do You Really Have To Put 20% Down When You Buy a Home?

Unless your specific loan type or lender requires it, odds are you won’t have to put 20% down. There are loan options out there designed to help first-time buyers like you get in the door with a much smaller down payment.

For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants, like Veterans. So, while putting down more money does have its benefits, it’s not essential. As The Mortgage Reports says:

“. . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . . the 20 percent down rule is really a myth.”

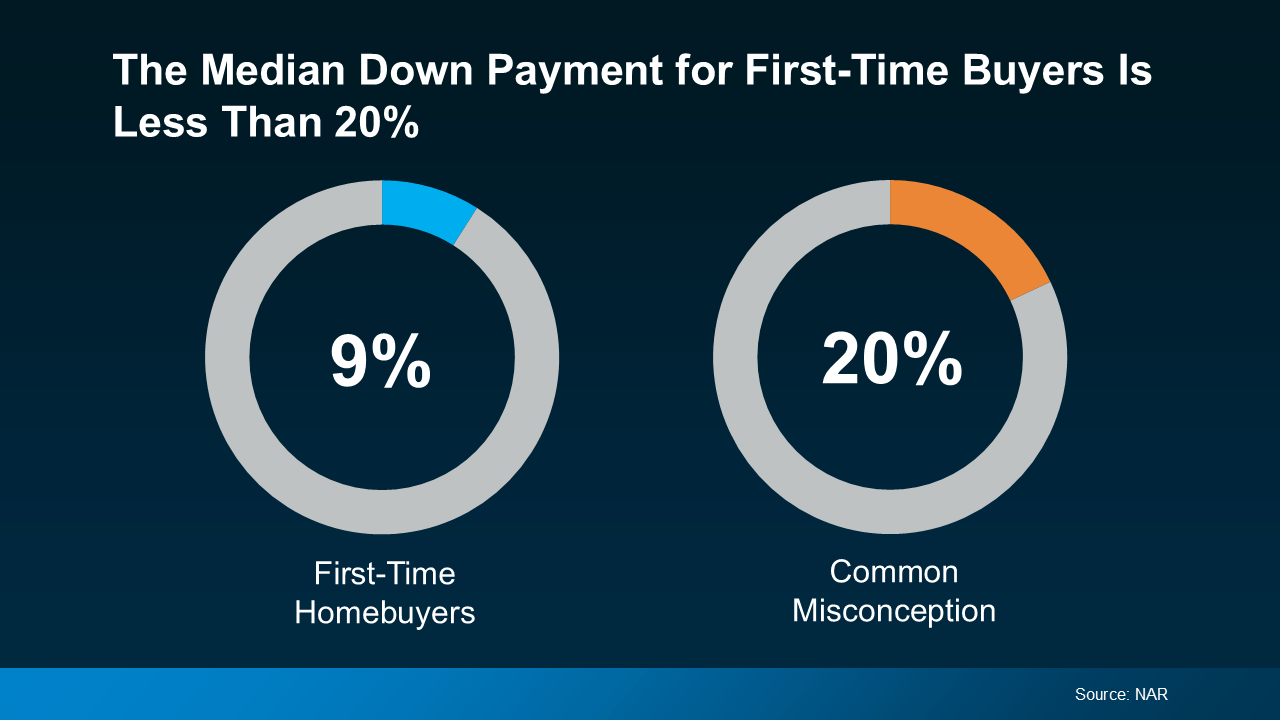

According to the National Association of Realtors (NAR), the median down payment is a lot lower for first-time homebuyers at just 9% (see chart below):

The takeaway? You may not need to save as much as you originally thought.

The takeaway? You may not need to save as much as you originally thought.

And the best part is, there are also a lot of programs out there designed to give your down payment savings a boost. And chances are, you’re not even aware they’re an option.

Why You Should Look into Down Payment Assistance Programs

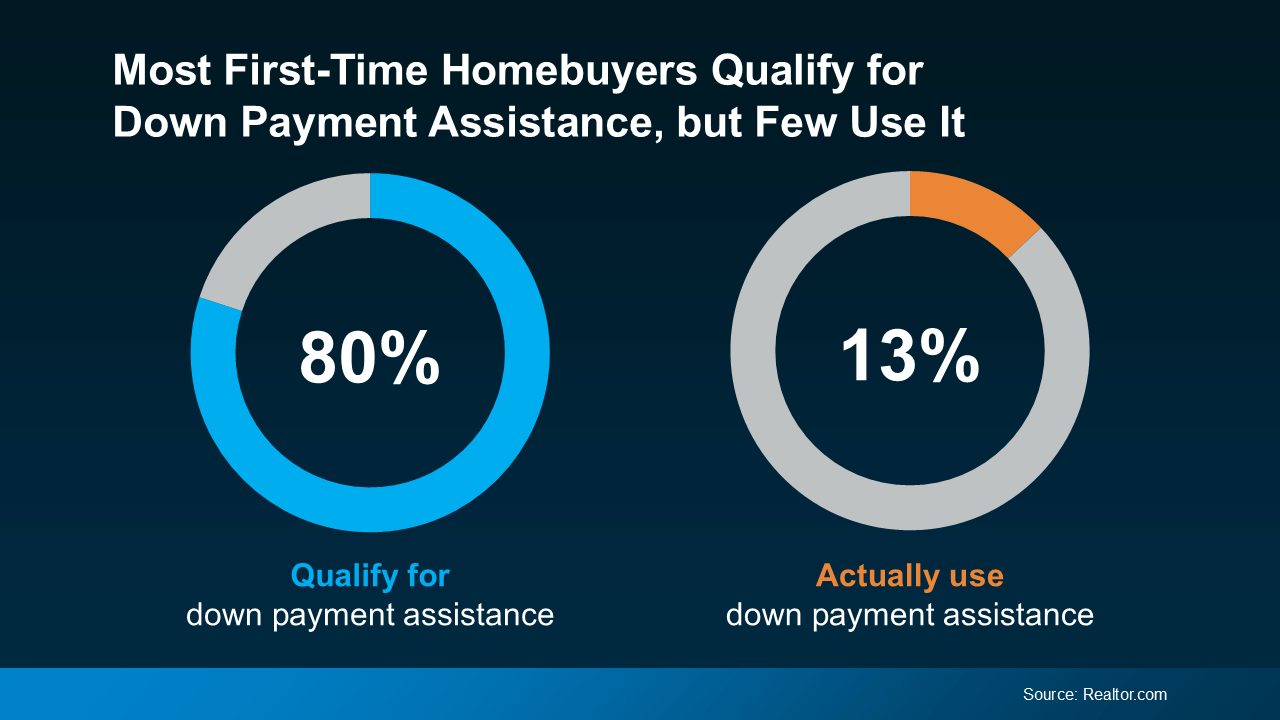

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

That’s a lot of missed opportunity. These programs aren’t small-scale help, either. Some offer thousands of dollars that can go directly toward your down payment. As Rob Chrane, Founder and CEO of Down Payment Resource, shares:

That’s a lot of missed opportunity. These programs aren’t small-scale help, either. Some offer thousands of dollars that can go directly toward your down payment. As Rob Chrane, Founder and CEO of Down Payment Resource, shares:

“Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.”

Imagine how much further your homebuying savings would go if you were able to qualify for $17,000 worth of help. In some cases, you may even be able to stack multiple programs at once, giving what you’ve saved an even bigger lift. These are the type of benefits you don't want to leave on the table.

Bottom Line

Saving up for your first home can feel like a lot, especially if you’re still thinking you have to put 20% down. The truth is that’s a common myth. Many loan options require much less, and there are even programs out there designed to boost your savings too.

To learn more about what’s available and if you’d qualify for any down payment assistance programs, talk to a trusted lender.

Learn why the 20% down payment for buying a home is a common misconception. Discover alternative options and strategies to buy a home with less upfront cost.

20% down payment myth, home buying myths, down payment options, affordable homeownership, buying a home with low down payment, mortgage down payment alternatives, real estate tips, first-time homebuyer advice, debunking home buying myths, home financing solutions.

Learn more:

The idea that you need a 20% down payment to buy a home is one of the most pervasive myths in real estate (Consumer Financial Protection Bureau), leading many potential buyers to delay their dreams of homeownership. Fortunately, experts like those at [NerdWallet](https://www.nerdwallet.com/) clarify that there are numerous low-down-payment options available, from FHA loans to VA loans ([Military.com](https://www.military.com/)). Programs like those offered by [Rocket Mortgage](https://www.rocketmortgage.com/) and [Bankrate](https://www.bankrate.com/) allow buyers to explore 3%-5% down payment solutions. Additionally, organizations such as [Down Payment Resource](https://downpaymentresource.com/) connect buyers with local assistance programs, while [Investopedia](https://www.investopedia.com/) explains the benefits of PMI for those putting down less than 20%. [Realtor.com](https://www.realtor.com/) highlights how location can influence the percentage required, and [Zillow](https://www.zillow.com/) offers tools to calculate affordability. [Redfin](https://www.redfin.com/) and [HomeLight](https://www.homelight.com/) provide further insights into down payment myths and real-world financing examples. Explore these resources to find the right path to your dream home.

Categories

Recent Posts